Customers demand timely shipments, quality products, and low prices. Fulfilling these requirements is easier said than done since manufacturers have to contend with skilled labor shortages, rising raw material costs, and complex supply chains. But that’s not all. Besides meeting ever increasing customer demands, manufacturers must also maintain profitability.

Hence, manufacturers need a sound strategy in place that includes optimal production schedules, smart pricing strategies, and reliable manufacturing inventory management software. A strong understanding of manufacturing expenses is at the core of all this.

The total manufacturing cost formula gives you a complete breakdown of all costs involved in manufacturing. Business leaders need this information to cut unnecessary costs, improve cash flow, and get the best value for money.

Table of Contents

Total Manufacturing Cost Defined

The total manufacturing cost (abbreviated as TMC) includes all expenses involved in manufacturing a product including scrapped items, work in progress, and finished goods.

TMC adds up 3 cost categories: manufacturing overhead, direct labor, and direct materials. Direct materials include raw materials and supplies needed for the end product. Direct labor has salaries, taxes, and benefits related to the manufacturing staff. Manufacturing overhead comprises all those expenses that are not directly related to the items manufactured, like utilities and maintenance.

For instance, a furniture manufacturing company will include factory rent, utilities and equipment maintenance under indirect expenses when calculating the TMC.

Key Takeaways

- Three main cost components comprise total manufacturing cost: manufacturing overheads, direct labor, and direct materials.

- Regular analysis of the TMC can reveal opportunities to make good investment decisions, allocate resources efficiently, improve pricing, enhance processes, and cut waste.

- TMC needs to be analyzed in addition to other key metrics like the cost of goods sold. This helps manufacturers improve different parts of their processes.

- TMC is based on many different data points that need to be accurate and complete for this key value to be useful.

- Manufacturing inventory management software and other related software solutions like accounting software can provide the necessary data to calculate TMC for decision making.

Gain full control over material cost and movement with our capable software.

Let’s Talk!Explaining the Total Manufacturing Cost

TMC is an important value that needs to be accurately determined for successful cost reduction. It should also be pointed out that while manufacturing overheads, direct labor, and direct materials are different from each other, they do have an effect on each other. This influences total manufacturing expenses.

For instance, if direct labor hours are reduced, this will reduce the total wages paid out but at the same time it will also bring down manufacturing output, causing reduced sales. Likewise, selecting better quality raw materials may raise direct materials costs, but it can also lead to an increase in product quality, thereby increasing sales and improving profits despite higher direct materials costs.

Why Calculating TMC is Vital

TMC gives you a holistic view of the overall costs involved in manufacturing. This in-depth analysis is the key link between operations management and financial control. Hence, it provides important metrics that finance, operations, and high-level executives can discuss for making good business decisions. With financial and operations management in sync, the manufacturer can formulate sound data-driven decisions. Precise TMC assessments form the basis for capital investments, resource allocation, production planning, and pricing strategies that drive higher profits.

Accurately assessing the TMC is vital for tracking various costs so that the manufacturer is informed about operational problems that need to be addressed for profitability, like increased material costs (stemming from supply chain problems for instance) or increased overhead costs (caused by faulty equipment, for instance). By monitoring key cost drivers, management can execute strategies for bringing costs down, like, for example, investing in reliable supply chain software or upgrading equipment.

TMC is a powerful tool to remain agile despite operational challenges, like changing customer demand, fluctuating materials costs, and logistics problems. For instance, the manufacturer can analyze its TMC to quickly identify viable alternate materials to maintain product quality (without incurring excessive costs) in case regular raw materials are in short supply.

Formula for the Total Manufacturing Cost

The formula for calculating the total manufacturing cost is quite straightforward.

Total Manufacturing Cost = Direct Labor + Direct Materials + Manufacturing Overhead

Only relevant manufacturing costs must be added but not nonmanufacturing costs, like sales commissions. Another key point is to avoid counting the same cost from different categories. For instance, if during the entire working week, the plant manager works two days on the assembly line and spends three days managing operations in another location, then 40% of their wages will be categorized as direct labor and the rest (60%) will be classified as manufacturing overhead since this is support work rather than direct labor.

Difference Between Direct and Indirect Manufacturing Costs

What is the difference between direct and indirect manufacturing costs?

The concept is very simple. Direct manufacturing costs are those that can easily be attributed to each manufacturing unit, for example direct materials and direct labor. For example, we can calculate the direct labor cost for each manufactured item as follows.

Direct labor cost per unit = time taken to produce each unit x hourly wage

Likewise, can calculate the direct material cost per manufactured item simply by adding up the costs of all raw materials and components that go into it.

Hence, determining direct costs is fairly straightforward.

But certain costs are harder to estimate for each unit. One such example is factory rent. It is not immediately obvious how much factory rent is to be assigned to each manufactured item. Another example is equipment depreciation. Again, it is not that easy to assign this amount to each unit.

That’s because these costs are generated indirectly via manufacturing.

Hence, they are called indirect costs or manufacturing overhead.

How to Calculate the Total Manufacturing Cost

So now that you have a good idea, how to calculate the total manufacturing cost?

Even though calculating the TMC seems pretty straightforward, errors can result if care is not taken. Each cost component should be determined accurately. To do so, relevant data needs to be collected from the manufacturing management software and different departments.

Since different data points need to be collected and they all need to be complete and accurate, using the right software solution is paramount for tracking costs reliably.

We will now go through all cost categories explaining how to calculate them and relevant cost cutting strategies.

Direct Material Costs

Direct material cost covers all expenses that can be tied directly to materials and components used in the manufactured product. For instance, when calculating the direct material costs for a bicycle model, we will have to add in the cost of each bicycle part such as seats, tires, gears, chains, frames, and add-ons.

In some cases, direct material costs may also include consumables and supplies that are normally categorized as indirect costs, like small tools and lubricants. Other such indirect costs can sometimes be included as well if they can be directly assigned materials, especially if they are significant, like storage costs, transit insurance, import duties, shipping, handing, and so on.

Tracking all such costs is essential for cost control since the manufacturer is aware of how much each manufactured unit costs in terms of direct materials. Besides tracking total and unit materials costs, analysts will also want to know the cost per batch or job.

Calculating Direct Material Costs

Here is the standard formula which gives you the direct material cost for a specific financial period.

Direct Materials Costs = Starting Raw Materials Value + Procurement costs of new materials – Closing Raw Materials Value

For example, a garments manufacturer begins the week with raw materials worth $100,000 (threads, fabrics, zippers, buttons, etc). The manufacturer then buys $250,000 in new raw materials during this time frame and at the end of this period has $80,000 worth of inventory. The direct materials calculation goes like this.

Direct materials cost = $100,000 + $250,000 – $80,000

= $270,000

The value of $270,000 represents the monetary amount of raw materials that was used to manufacture garments during the said time frame.

Note that besides the amount purchased, the final and starting inventory are factored in for a realistic figure. Making this distinction is vital since the material used in production is not necessarily the material purchased during this time period. That is, production does not just consume what was procured during this period, in fact, it can also include the preexisting stock. Plus, some material purchased may not be consumed during this period – this might end up as the closing stock. In short, you should adjust for closing and opening stock to accurately reflect the actual inventory consumed and thus the actual direct material cost.

Reducing Direct Material Costs

Raw material costs are rising each year. Hence, serious steps are needed to reduce rising costs so that manufacturers can stay competitive. Here is what can be done.

- Find Better Rates: Source raw materials from lower cost suppliers who provide the same quality at lower rates.

- Negotiate: Talk to suppliers for bulk discounts and early payment discounts as well.

- Streamline Design: Improve product designs so that each manufactured unit requires fewer components and raw materials.

- Process Improvement: Analyze all processes to drive efficiency and minimize waste.

- Supply Chain Strategy: Monitor market conditions and update your production, procurement and supply chain strategy to ensure lower costs and timely shipments of raw materials.

- Manufacturing Inventory Software: the right software for manufacturing inventory tracks all raw materials, components, work in progress, and finished goods, so you know precise materials costs.

Our cutting-edge manufacturing inventory software gives you full visibility over all materials.

Talk with Experts!Direct Labor Costs

Direct labor costs cover the following:

- Part-time and full-time wages of production workers.

- Benefits of all kinds, such as paid leaves, retirement contributions, and health insurance.

- All tax payments at both the state and federal level, such as unemployment taxes, Medicare, and social security.

Direct labor costs may not vary in direct proportion with production volume. For example, when production slows down due to seasonal demand shifts, there may be less workers involved in production. However, there is a certain fixed level of the workforce that will be employed even with low demand so that skilled workers can be retained.

Calculating Direct Labor Costs

Here is the basic formula to calculate direct labor costs.

Direct labor costs = (Amount of hours worked x hourly rate) + taxes + benefits

For instance, if a certain manufacturer has 50 employees on its production line who each work 160 hours a month for $25 per hour, which includes taxes and benefits at a rate of 30 percent of the basic pay, then here is how direct labor cost is calculated.

Total hours worked = 160 hours x 50 workers = 8,000 hours

Basic pay for all workers = 8,000 hours x $25 per hour = $200,000 per month

Taxes and benefits for all workers = $200,000 x 30% = $60,000

Direct labor costs = $200,000 + $60,000 = $260,000

Payroll software is often used to keep track of all paid leaves, contractor payments, overtime, and basic pay. Direct labor costs can also be categorized by different product types to understand how labor costs are being distributed.

Reducing Direct Labor Costs

There are several ways to bring down direct labor costs, for example, by improving productivity, reducing idle time, and improving labor allocation. Here is what can be done in this regard.

- Cross-Training: Expanding the skillset of your staff improves labor flexibility, reducing downtime and dependence on costly specialists.

- Automation: Automating recurring manual tasks.

- Streamlining Processes: Improving the factory floor layout and all different processes to cut down on unnecessary material usage and worker movement.

While reducing direct labor costs is important, it is equally important to ensure that these cost-cutting measures don’t negatively impact worker satisfaction or product quality. Surveys often show that retaining talented employees and improving workforce productivity are among the top concerns for manufacturers.

Manufacturing Overhead

Manufacturing overhead is a term that encompasses all those production expenses that are not directly tied to the manufactured products but are nevertheless essential for running operations. Think of it as all production costs that do not fall under direct materials or direct labor costs. Here are some examples to give you a better idea.

- Building Costs: taxes, utilities, and rent for manufacturing facilities

- Indirect Labor: maintenance staff, logistics team, supervisors, and managers

- Equipment Costs: repairs, maintenance, and depreciation

- Supplies: that can be directly assigned to manufactured items – safety equipment, small tools, cleaning supplies

- Other Indirect Costs: Payments to insurance carriers and consultants

Unlike direct labor and materials costs, manufacturing overheads often remain constant despite changes in production volume (like rent and depreciation). Do note that there are some manufacturing overhead costs that can change according to production output, like utility bills.

How to Calculate Total Manufacturing Overhead Cost – Total Indirect Manufacturing Cost Formula

How to calculate total manufacturing overhead cost? You can do that with the total indirect manufacturing cost formula.

Manufacturing Overhead = Indirect Labor + Indirect Materials + Other Indirect Costs

For instance, a manufacturer incurs the following costs each month: $20,000 (maintenance and cleaning supplies), $80,000 for indirect labor (maintenance staff and supervisors), and $150,000 for other factory costs (insurance, utilities, and rent). The manufacturing overhead will be:

Manufacturing Overhead = $150,000 + $80,000 + $20,000 = $250,000

Manufacturing overheads are usually allocated according to different categories, like per labor dollar cost, per machine hour, per manufactured unit, and so on. Such allocation enables good pricing strategies and realistic product costing. Here is how the overhead rate is calculated for a given allocation base.

Overhead Allocation Rate = Total manufacturing overhead / Allocation base

So if the plant is manufacturing 500,000 units each month, then the overhead cost for each unit will be as follows.

Overhead Allocation Rate = $250,000 / 500,000 units

= $0.5 per unit

What this means is that each unit manufactured produced an additional $0.5 in overhead costs.

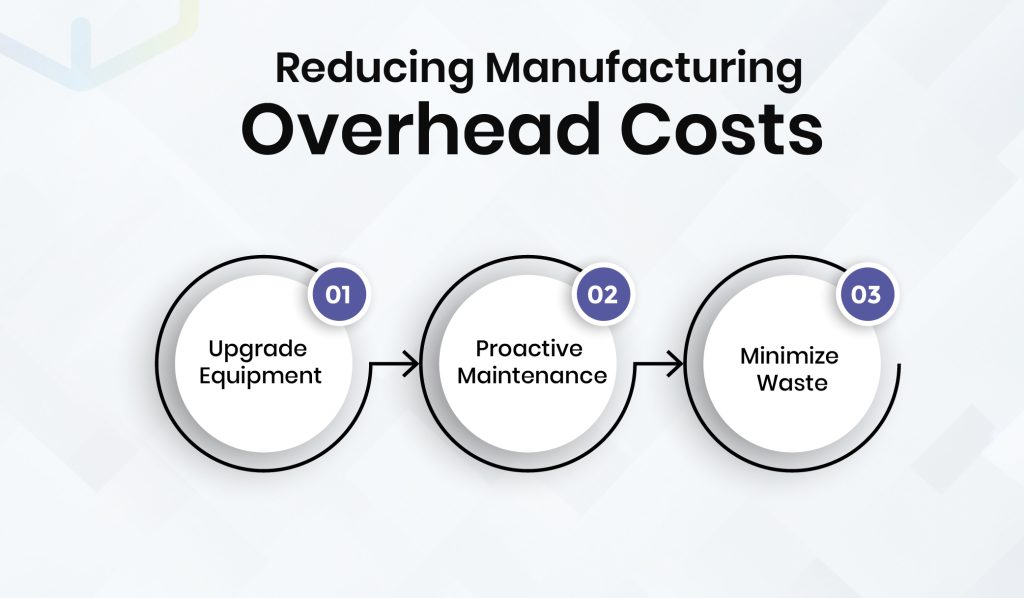

Reducing Manufacturing Overhead Costs

Manufacturers often try to bring down overhead costs by enhancing resource management and improving facilities. Here are some ways of doing this.

- Upgrade Equipment: Energy-efficient and reliable models reduce utility and maintenance costs.

- Proactive Maintenance: Carrying out proactive maintenance using an optimized maintenance schedule to prevent equipment breakdowns that require costly repairs and that result in costly disruptions.

- Minimize Waste: Track the use of safety equipment, cleaning supplies, and small tools to reduce waste.

There are some overhead costs that are not easy to reduce. For example, insurance costs and rent. To cut costs like these, big decisions are needed that may not be easy to implement, like changing factory location to benefit from lower rent and finding an insurer that charges less while offering reliable service.

Total Direct Manufacturing Cost Formula

The total direct manufacturing cost formula is as follows.

Direct manufacturing cost = Direct labor + Direct materials

Note that the direct manufacturing cost does not include manufacturing overhead – just direct costs.

Total Manufacturing Cost – An Example

Assume that a medical device maker manufactures 10,000 heart rate monitors each month. The monthly breakdown of all manufacturing costs is like this.

| Direct material inputs | Beginning raw materials inventory | $200,000 |

| Procurement purchases | $450,000 | |

| Ending raw materials inventory | $150,000 | |

| Direct labor inputs | Total direct staff | 40 workers |

| Average wage | $30/hour | |

| Average working time | 160 hours | |

| Benefits and payroll taxes | 35% of wages | |

| Manufacturing overhead costs | Indirect supplies and materials | $25,000 |

| Indirect labor | $90,000 | |

| Rent, utilities, insurance, and depreciation | $175,000 |

Step 1: Add up all direct materials costs.

Direct Materials Cost = opening raw material inventory + Procurement cost for new materials – closing raw materials inventory

Direct materials cost = $200,000 + $450,000 – $150,000 = $500,000

Step 2: Add up all direct labor costs.

Direct labor costs = (Total hours worked x hourly rate) + taxes + benefits

Total hours worked = 160 hours x 40 workers = 6,400 hours

Basic pay for workers = (6,400 x $30 per hour) $192,000 per month

Benefits and taxes for workers = $192,000 x 35% = $67,200

Direct labor costs = $192,000 + $67,200 = $259,200

Step 3: Calculate manufacturing overhead by adding all its components.

Manufacturing overhead = Indirect labor + Indirect materials + Other indirect costs

Manufacturing overhead = $25,000 + $175,000 + $90,000 = $290,000

Step 4: Add up all 3 cost components to find out the TMC.

Total Manufacturing Cost = Direct labor + Direct materials + Manufacturing overhead

Total Manufacturing Cost = $500,000 + $259,200 + $290,000 = $1,049,200

Benefits of Calculating the TMC

Tracking and accurately calculating the total manufacturing cost can give the manufacturer a powerful competitive edge in pricing, profitability, and efficiency. But for this to happen, it is vital to have a powerful manufacturing system at the core, like WareGo’s manufacturing inventory software so that collecting necessary data points is easier.

Track inventory costs and movement effortlessly with our software.

Start FREE Trial!Here are some benefits that manufacturers gain by accurately tracking the TMC.

Better Cost Control: Accurate TMC figures enable accurate costing. For example, a precise TMC figure can be broken down across different production lines to find out how much each production line is incurring in terms of cost. Doing so lets you identify costly processes that need to be improved for cutting costs.

Identifying Waste: Monitoring the TMC accurately means you can find out which areas are undergoing rising costs. You can then pinpoint bottlenecks, inefficiencies, and waste to remedy such problems.

Manufacturing Insights: Tracking changes in the TMC allows managers to uncover patterns that influence profitability, like seasonal changes in labor costs or shifts for manufacturing volume. Leaders can then make informed decisions using these insights for better resource allocation, scheduling, batch sizes, forecasts, and budgets.

Improved Financial Visibility: Regular TMC analysis gives you full visibility into all parts of the manufacturing workflow so that you can make strategic decisions as well, like validating capital investments.

TMC vs Cost of Goods Sold (COGS)

Although they are strongly related, both COGS and TMC have different purposes. TMC encompasses all costs related to manufacturing during a given time frame, including the discarded stock, unsold goods, and work in progress. Hence, TMC is different from COGS which only considers finished goods that are sold.

For instance, if a manufacturer has a TMC of $1,000,000 for the month, but is only able to sell just 80% of the units produced, then the COGS will be $800,000. In certain situations, the difference between TMC and COGS will be greater, for example, during seasonal shifts, when the manufacturer uses slow seasons to store more inventory. In this situation, the organization may experience a rise in TMC but not in the COGS, leading to a widening gap between these figures. However, during peak seasons, when demand is higher, the difference between TMC and COGS will be smaller since the company is selling more inventory.

Comparisons between COGS and TMC are important for assessing the rate at which goods are being sold. This matters especially when products have a short shelf life or the demand is volatile.

TMC vs COGM (Cost of Goods Manufactured)

The Cost of Goods Manufactured (or COGM) includes all goods that are manufactured within a specific time period – however, it includes finished goods only, not work in progress. COGM is different from COGS since it covers the cost of all finished items, including unsold items.

Here is how to find out the COGM.

Cost of goods manufactured = TMC + Beginning WIP – Ending WIP

Note that WIP stands for work in progress (or unfinished goods).

Suppose an organization has a TMC of $1,000,000 for the month. The starting WIP value is $300,000, while the ending WIP value is $250,000. Then,

Cost of goods manufactured = $1,000,000 + $300,000 – $250,000 = $1,050,000

If the COGM value is greater than the TMC, it means that certain manufactured items were made in the previous financial time frame. If the COGM value is less than the TMC, then it means that the organization has a larger stock of WIP now than it had previously. Hence, these figures are useful for estimating the inventory trends in addition to costing.

Summarizing

Finding out the total manufacturing cost is crucial for bringing down costs to a minimum. But that is not possible without reliable manufacturing inventory software to monitor all inventory in real-time.

WareGo gives you complete visibility over the movement of all inventory, including raw materials, parts, work in progress, finished goods, and supplies. Reports and analytics give you powerful insights for bringing costs down.

You have come to the right place! Master inventory cost control with our software.

Book FREE Demo!FAQs

How do you calculate the total cost of production?

Total Cost of Production = Direct labor cost + Direct materials cost + Manufacturing overhead

What is the formula for total cost?

Total Cost = Total Fixed Costs + Total Variable Costs

What is an example of a total manufacturing cost?

Here is an example of total manufacturing cost.

Suppose

Direct materials Cost = $12,000,000

Direct labor cost = $2,500,000

Manufacturing overhead = 500,000

Then the total manufacturing cost turns out to be

TMC = Direct materials cost + Direct labor cost + Manufacturing overhead

= $12,000,000 + $2,500,000 + $500,000

= $15,000,000

How to calculate TMC?

You can calculate TMC by adding up all direct materials, direct labor, and manufacturing overhead costs.

TMC = Direct labor cost + Direct materials cost + Manufacturing overhead